Have you ever have your dream house? I’m sure a lot of people have a dream to own their own house. But, since we are young, we mostly clueless about how to buy your own house. Well, this Twitter user decided to share some knowledge about buying a house that garnered over 10K likes and 6K shares

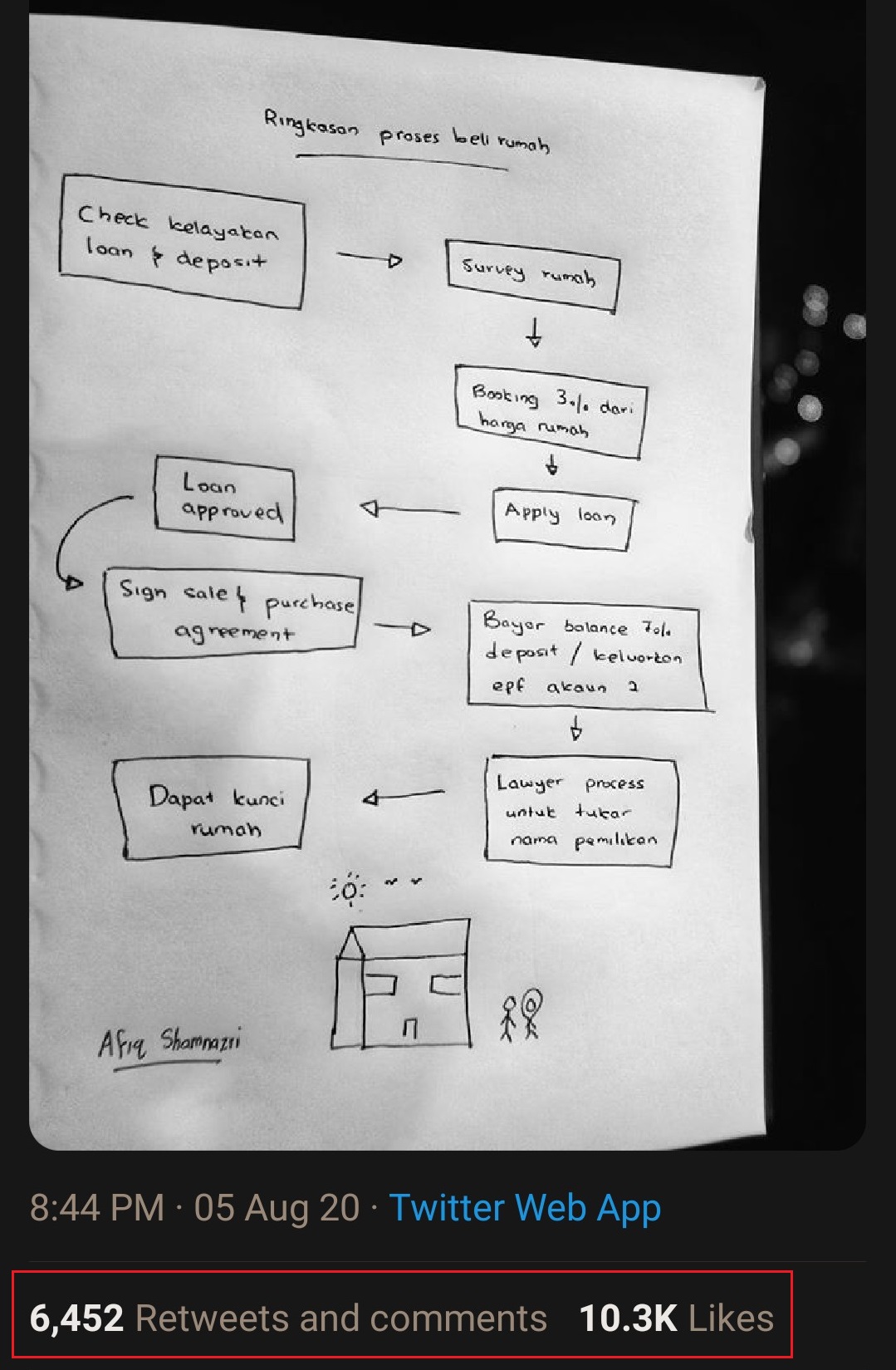

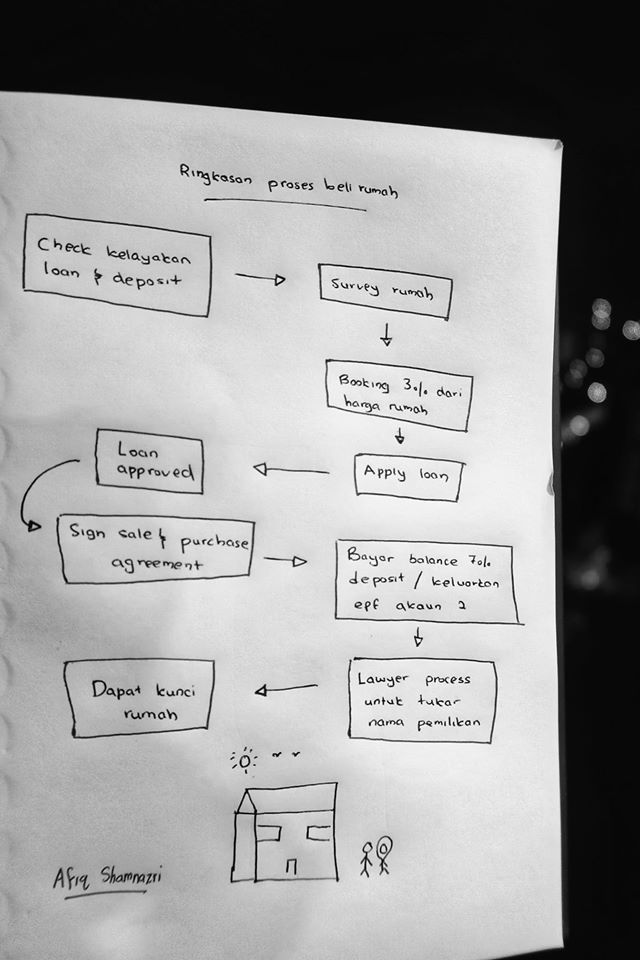

We break the flow process into three which are inventory phase, purchase phase, and name change phase. First, he started with the inventory phase which means you have the intention of buying a house. You have to start by checking how many home loans you can take. It is a critical part but if you thinking about buying using cash, then you can skip this part.

The bank will see these 3 things in order to approve or reject our loan, which are income, CCRIS, and Scoring. For income, the bank will calculate DSR (Debt Service Ratio), the percentage of the loan that you can take according to your salary. As an example, your salary is RM3000, then have a loan RM1500 monthly commitment so your DSR will be 50%. If more than a certain percentage of DSR, the loan may be rejected. The more salary, the bigger the percentage of DSR that you can take.

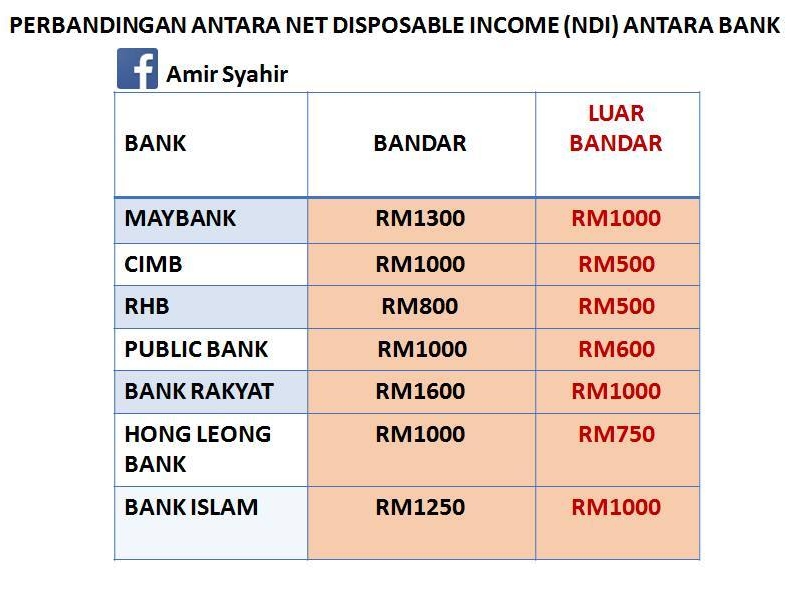

The term is NDI (net disposable income). If your salary over RM3000, you deduct all your new and old commitments. Then, there must be at least RM1000-RM1200 (Different depending on the bank) can be released. An example is in this picture is not up to date but just to give you the idea. The formula to calculate DSR to buy a house is old commitment + monthly commitment of new house to buy / net salary x 100.

A document that the bank wants are a copy of your identification card, payslips, bank statements, EPF, and employment letter. You can ask your agent for help regarding this. Extra tips for loans are that each bank has its own package and the criteria are different. So you can survey yourself which bank is right for you. There will be no best bank but only a suitable bank. Bank DSR calculations are also different.

The next one is about the deposit, costs involved in buying a home, It is best if you can provide 15% of the house price. Example of a house priced RM200,000, you get ready with RM30,000. This is the best-case scenario if it can be provided, it is good, but if it is not enough, is it okay? Yes. Another option for a 10% deposit is to use EPF account money. You can withdraw 10% of the house price or all at once (whichever is lower). Another option if you want to buy a house with a minimum deposit is to buy a new project. Each project has developed packages that help reduce deposits. Other fees that buyers have to prepare are lawyer SNP fees, loan lawyer fees, valuer, and insurance.

After knowing how much loans you can take, the last thing to do is you have to make a plan. Plan about that house. Things to think about are you want to sit alone or rent, the period of staying if in another 5 years you want to buy a new house or are you having another plan to get married in near future. Because when you take a loan. A commitment must be paid every month. Your expenses will also change a little. After you have a proper plan, then you have settled the first phase which means you are ready to buy a house.

Now it is the purchase phase. When this purchase phase, you will window shopping. Refer back to the ‘plan’ that you made during the preparation phase. Find a house that matches the criteria you want. Not everyone can have a few that match is okay.

After found a house that you want, book it to proceed with the next step. Booking money must be to the property agency or law firm (third party) even if you buy from relatives, neighbors, acquaintances. Because the property agency or lawyer will act according to the standard conduct by the Board of Assessors and Real Estate Agents (LPPEH).If the loan rejects standard conduct will be fully refunded.

The booking amount is 3.18% of the price of the house. If you are already paid for the booking and the owner has signed, attached the form with the document for the loan, submit it to the bank to apply for a loan. Some agents will help you do this. If the documents are all completed within a week, you can get approval for a loan. If the loan has been approved, the agent will inform the lawyer to prepare a sale and purchase agreement (SNP). Within 2 weeks, you can sign. When you sign the SNP, you have to pay the balance. Booking has paid 3% so there is another 7%. If you want to use EPF, you do not need to pay for this thing. For freehold house after sign SNP, you can continue to take out EPF. If the leasehold house, you have to wait for consent first.

The name change phase you relax because many lawyers do the work. For a freehold’s house, it usually takes 3-4 months. As for leasehold’s house, it is 6 months to a year. If the house is lowcost, it might be a little late because of the need to ask for consent. What you have to do is just follow up once a month near the processor. Do not want to upset lawyers because this process is not one party. 2 or 3 parties involved.

There will be one time the bank that we apply for a loan will release a certain amount of money to the acc bank home loan owner (if the owner still has a debt). The term is the first disbursement. This is a regular bank procedure. If we sell a house, the bank will close our debt first, then finally we will be able to get our net money.

At this time the house still belongs to the owner because the owner can not get the money anymore. There are a few processes before the bank releases all loan balances. So when all the lawyers have settled, they will call to see the house. You will see the house. Check for doors and other things. if everything is okay, you can get the key from the lawyer. After getting the key, there is one last thing to do, which is to change the name near the water bill, electric, Indah Water, maintenance, assessment tax. Usually this first house you must love a little more.

Netizens’ Responses

This information for all of you who wanna buy a house~

Info via Twitter