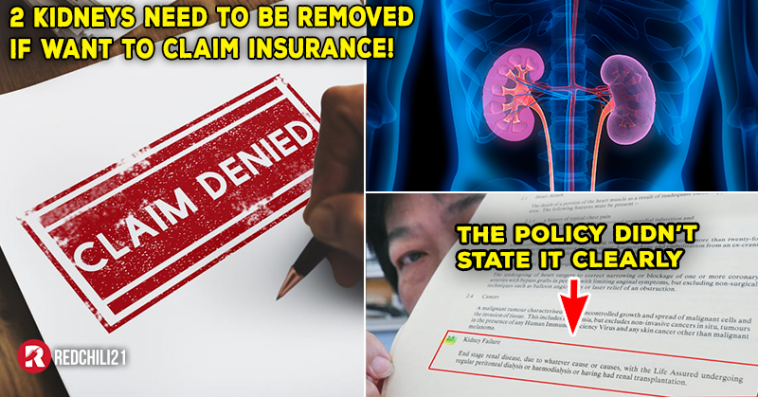

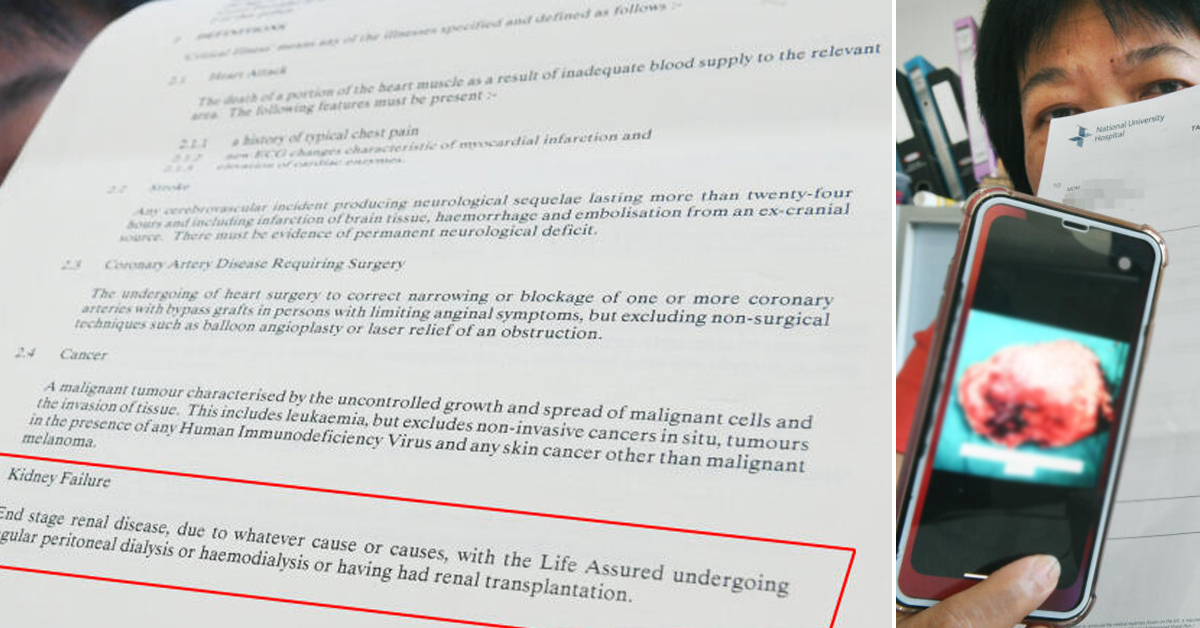

“Due to kidney failure, my wife had to remove one kidney, but i was told by the insurance company it’s not claimable for just removing 1 kidney. Only if you remove 2. But can someone live without 2 kidneys?”

Businessman in Singapore, known as Mr. Xu, 67-year-old said a female insurance agent sold him the insurance policy about 20 over years back. He get himself and his family insured, covered with life and medical insurance, reported by Oriental Daily.

“When the insurance agent sold me the insurance said we are covered with 30 disease. Believing in her as she is my business partner’s wife. So, we didn’t ask in details.”

However, 25 years later, my 61-year-old wife was diagnosed with kidney stone on May 2020. Further medical checks found one of her kidney was malfunction. She need to undergo surgery to remove it.

She was hospitalised for 21 days. During her hospitalisation, Mr. Xu contacted his insurance agent to arrange for the insurance claim. They filled up forms and provided all necessary documents for the submission. However, the insurance company turned down their application.

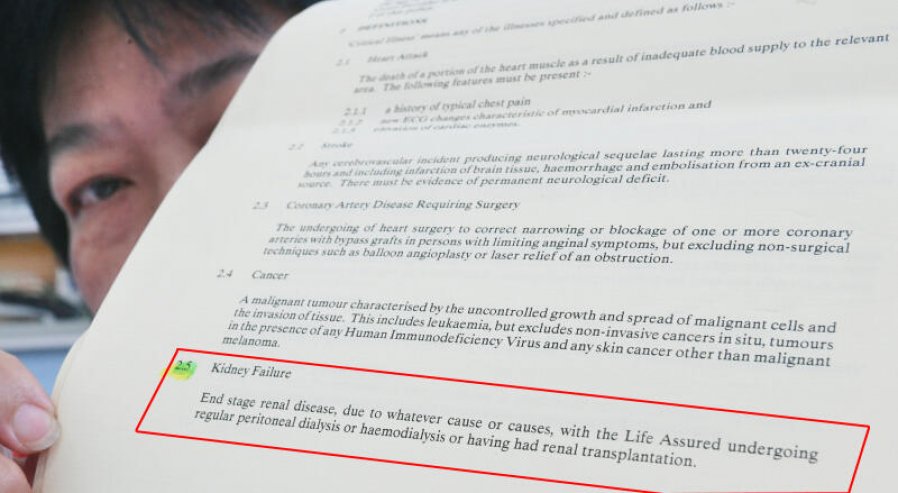

” The agent told me only if 2 kidneys removed then only i’m eligible for the claims but i wonder how someone could live without 2 kidneys? and the clause mentioned in the policy is very vague without saying 1 or 2 kidney to be removed only entitled for the claim.”

Mr. Xu’s wife underwent 2 surgeries with total hospitalisation bill cost SGD 30,000 (RM 90,000) after government subsidiary, Mr. Xu still need to pay SGD 9,000 (RM27,000) from his own pocket.

Mr. Xu urged public do not blindly purchase any insurance policy but understand clearly what’s the details in the insurance policy.

{kind=link}

Redchili21 contacted Nigel Teo, a Life insurance adviser who is 10 years in the industry said it’s advisable to review insurance policy on yearly basis as insurance company will review and update the clause based on current medical and healthcare conditions.

To elevate health protection, most of the insurance company in the market launched some innovative plan to cover even early diagnosis of certain illness too.

However, beside policy for critical illness, it’s important for one to have a medical card which can cover the cost for hospitalisation in case of emergency.